Retirement Planning Made Simple

Retirement may feel like a distant goal, but the earlier you start planning, the more secure and comfortable your future will be. Retirement planning is about ensuring that you achieve financial independence when you stop working, allowing you to live your later years with freedom, dignity, and peace of mind.The first step in retirement planning is to estimate your future expenses. Consider not only day-to-day living costs but also healthcare, lifestyle choices, travel, hobbies, and the inevitable impact of inflation over time. Understanding these future needs will give you a realistic, personalized target for the corpus you need to accumulate before retirement. Financial experts often suggest aiming to save between 70% and 90% of your pre-retirement income to maintain your standard of living.

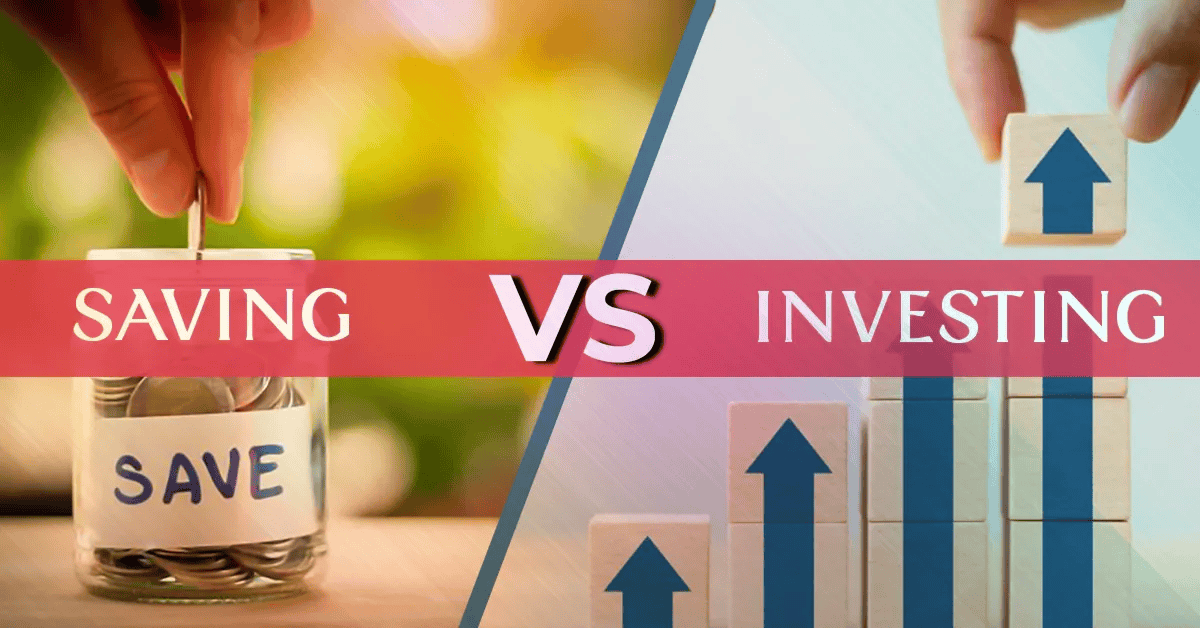

Next, it’s essential to contribute regularly to retirement accounts. Depending on your country, options may include the Public Provident Fund (PPF), Employee Provident Fund (EPF), 401(k), IRAs, pension plans, or other long-term savings schemes. The key is consistency: making regular contributions—even modest amounts—can accumulate significantly over time, thanks to the exponential power of compounding. Starting early is your most significant advantage; it means your money has decades to grow, significantly reducing the burden of higher contributions later in life. For instance, a 10-year delay in saving can potentially halve your total accumulated corpus by retirement age.

Diversifying your investments is another critical principle. A mix of assets like stocks, bonds, real estate, and other instruments helps balance risk and reward, ensuring your retirement corpus is resilient against market fluctuations. Your asset allocation should be a dynamic strategy that shifts with your age. Younger investors with a long time horizon can afford a higher exposure to growth-oriented equities (often or more) to maximize returns. As you move closer to retirement (your 50s and 60s), the focus should gradually shift to capital preservation and income stability, prioritizing safer, fixed-income instruments like bonds or annuities, with equity exposure often reduced to

–

to minimize the impact of short-term market volatility.

Retirement planning is not just about money—it’s about freedom and lifestyle. It allows you to travel, pursue hobbies, spend quality time with family, or even explore new ventures without financial stress. The ultimate goal is to create a retirement where you can live on your own terms, rather than being constrained by financial limitations or forced to work. A well-funded retirement also provides a crucial financial safety net against rising healthcare costs and unforeseen expenses.

Failing to plan for retirement is essentially planning to fail. The best gift you can give yourself is a well-thought-out strategy that ensures a comfortable, secure, and independent future. By starting early, contributing consistently, diversifying wisely, and leveraging the power of compounding over a long investment horizon, you set yourself up to enjoy your retirement years with confidence and peace of mind. Regularly review your plan, at least annually, and adjust your savings and investment mix to stay on track for your desired financial independence.

Next, it’s essential to contribute regularly to retirement accounts. Depending on your country, options may include PPF, EPF, 401(k), IRAs, pension plans, or other long-term savings schemes. The key is consistency: making regular contributions—even modest amounts—can accumulate significantly over time, thanks to the power of compounding. Starting early means your money has more time to grow, reducing the burden of higher contributions later.

Diversifying your investments is another critical principle. A mix of stocks, bonds, real estate, and other assets helps balance risk and reward, ensuring your retirement corpus is resilient against market fluctuations. For younger investors, higher exposure to equities can maximize growth potential, while those closer to retirement may prioritize safer, fixed-income instruments to preserve capital.

Retirement planning is not just about money—it’s about freedom and lifestyle. It allows you to travel, pursue hobbies, spend quality time with family, or even explore new ventures without financial stress. The ultimate goal is to create a retirement where you can live on your own terms, rather than being constrained by financial limitations.

Failing to plan for retirement is essentially planning to fail. The best gift you can give yourself is a well-thought-out strategy that ensures a comfortable, secure, and independent future. By starting early, contributing consistently, diversifying wisely, and leveraging the power of compounding, you set yourself up to enjoy your retirement years with confidence and peace of mind.